Sending Money to Ethiopia? A Diaspora Guide to Hawala & The Hidden Risks

Ethiopia hawala. Let’s talk about it.

****

Her trip to Phuket was booked. She was now waiting in a major bank to be served. She wanted money to travel, but that was not easy. She sounded stressed and kept sending me Whatsapp messages about the long line and difficulty to obtain forex. She had been waiting since morning. It was now 5pm and she hadn’t succeeded.

They asked her to provide a support letter, asked who sent the money, why she needed the money, and where she was headed to. After spending the whole day at the bank she was asked to return the next day. We had to change the flight at added costs.

The next day she was given $200, hardly enough for emergency. Without the dollars she could not enter Thailand. The bank said it was all they could get. The rate was higher than the prevailing market rate. Both Amen and I were disappointed. I even thought about giving her my Wise Bank Card to use in Ethiopia but how would I? I was in Thailand, and Thai immigration wanted to see that she had the cash (not card).

This experience made me research about forex remittances in Ethiopia, and whether it could be a business opportunity given the high demand for forex. It is how I stumbled upon the Ethiopian Hawala system.

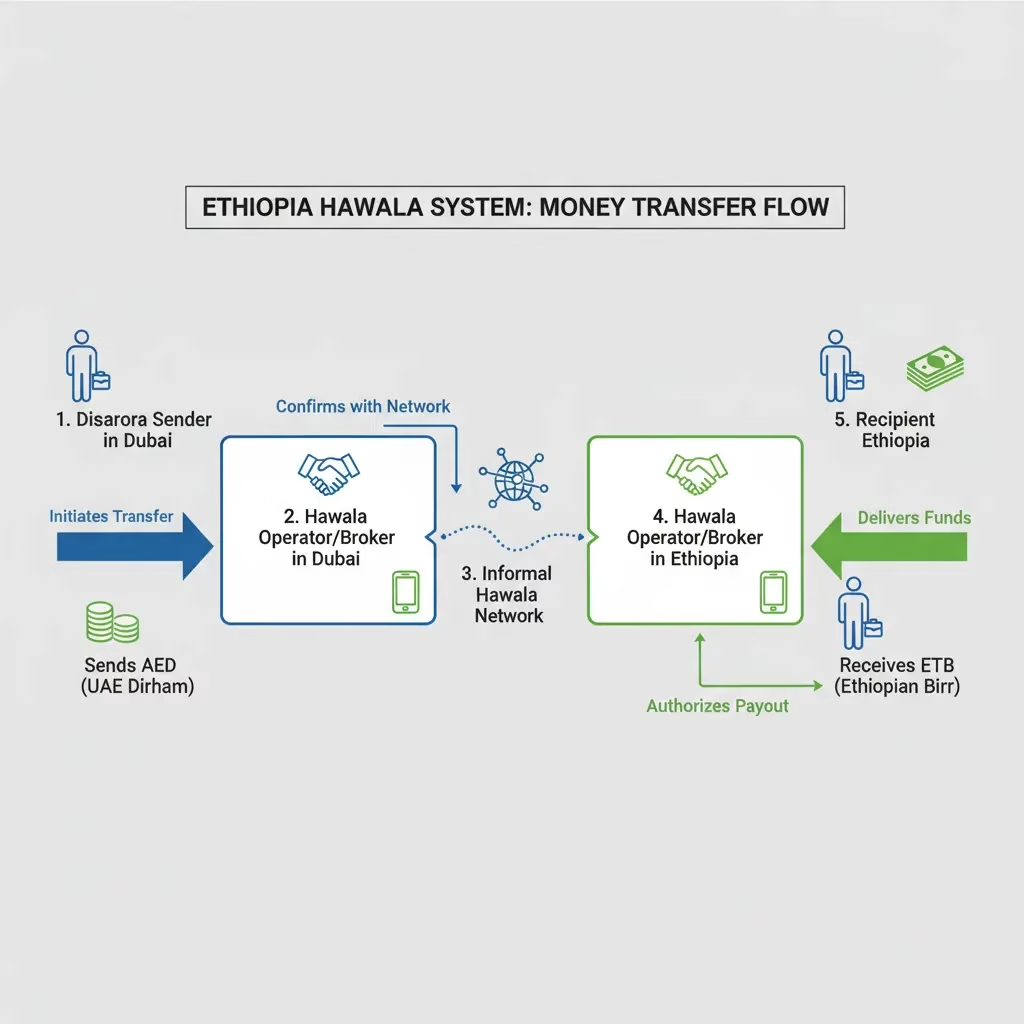

Ethiopia Hawala: What is the System and Why is it Popular?

At its heart, Ethiopia Hawala is a system built on trust. It operates outside the formal banking world. Here is a simple breakdown of how it typically works:

- You give foreign currency (e.g., US Dollars) to an informal agent in your city, say London or Washington D.C.

- This agent contacts their counterpart in Ethiopia, perhaps in Addis Ababa or Gondar.

- The Ethiopian agent then pays your family or friend the equivalent amount in Ethiopian Birr, often at a rate much higher than the official bank rate.

No money physically crosses borders. It is a ledger of debts and credits between agents. The appeal is clear: a better exchange rate means more Birr in your loved one’s pocket. For decades, this has been a common practice. However, the landscape in Ethiopia is changing dramatically, and what was once common is now actively prosecuted.

“The Ethiopian government, through its ‘Digital Ethiopia 2030’ strategy, is on a mission to create a modern, transparent, and formal digital economy. Informal systems like Hawala directly undermine this national goal, which is why the crackdown is so severe.”

Understanding the Risks of Ethiopia Hawala

The ‘Ethiopia Hawala’, an informal money transfer system, is used to transfer money in and out of the country without following the stringent exchange control market. They often promise better exchange rates and convenience, a tempting offer when you want to make every dollar, pound, or euro count. But just as a wise elder advises, “A path that seems too short can sometimes lead to a long regret.”

This path, my friends, is fraught with hidden dangers that can turn a beautiful trip into a distressing ordeal.

Diaspora Money Transfer Ethiopia: Why You Must Avoid Informal Transfers

Using an unlicensed money transfer system is not just a minor infraction; it is a direct violation of Ethiopian law. The National Bank of Ethiopia (NBE) is the sole authority regulating foreign exchange, and it has made its position crystal clear. Engaging with the black market, even as a sender, puts you and your recipient at significant risk.

Ethiopia Forex Black Market: A Direct Warning from the National Bank of Ethiopia

In late December 2025, the NBE issued a stern public notice, warning the global Ethiopian diaspora to send money exclusively through licensed money transfer agents. The notice explicitly states that using unlicensed agents and illegal Hawala networks is prohibited and can cause severe disruptions and legal consequences for recipients.

Let’s break down the specific legal and personal risks you face.

1. Violation of Ethiopian Law

The primary law you risk breaching is the Foreign Exchange Directive No. FXD/01/2024. This directive, along with the “Prevention and Suppression of Money Laundering and Financing of Terrorism Proclamation,” makes it illegal for any person or entity to conduct money remittance services without a license from the NBE. When you use an informal agent, you are participating in an illegal financial transaction.

- For the Sender: While you are abroad, your direct legal risk is lower. However, if you travel to Ethiopia, any connection to these transactions can create serious problems.

- For the Recipient: Your family or friend in Ethiopia bears the most immediate risk. They can face investigation, have their bank accounts frozen, and even face prosecution for receiving funds through illicit channels.

2. Frozen Bank Accounts and Confiscation of Funds

This is not a theoretical threat. The Ethiopian government is actively monitoring and cracking down on these activities. The Financial Intelligence Service has become highly effective at identifying suspicious patterns.

- August 2025: The bank accounts of 138 individuals were frozen as part of a crackdown on illegal foreign exchange markets. Authorities stated these individuals were under surveillance for treating illegal forex dealings as a routine business.

- November 2025: In an even larger operation, authorities arrested 112 people and froze 519 bank accounts linked to informal cross-border currency transfers and money laundering.

Imagine your loved one’s shock and distress when they find their bank account, containing their legitimate savings, is suddenly frozen because of a transfer you sent. The process to unfreeze an account is lengthy, difficult, and not guaranteed to succeed.

3. Risk of Fraud and Complete Loss of Money

The Hawala system operates on trust, but that trust can be broken. Since there is no legal contract or formal recourse, if the agent in Ethiopia fails to pay your recipient, your money is simply gone. You cannot report the theft to the police because you would be admitting to participating in an illegal activity yourself. You are left with no protection.

4. Association with Criminal Activity

Informal money transfer networks are often exploited for more sinister purposes, including money laundering and the financing of terrorism. By using these channels, you could unintentionally become a link in a chain of serious criminal activity, attracting the attention of both Ethiopian and international law enforcement agencies.

The Government’s Stance: Recent Actions and Banned Operators

The Ethiopian government’s warnings have been backed by decisive action. The NBE has not only targeted individuals but has also publicly named and banned international operators facilitating these illegal transfers.

Banned and Unlicensed Operators

The NBE has explicitly warned against using several unlicensed operators. In August 2025, it banned four US-based firms. More recently, in late 2025, it published a list of unlicensed agents that included:

- Shgey Money Transfer

- Adulis Money Transfer (ADZ)

- Red Sea

- Avanti

- World Direct Link

- Rasmy Pay

- USwyre

- Zola

- Taaj Financial Services

Using any of these or other unlisted, unlicensed services is a high-risk gamble.

Governor Eyob Tekalign has been unequivocal, stating that the NBE will take “strong enforcement measures” against illegal operators, particularly those based in hubs like Dubai, who are seen as deliberately distorting Ethiopia’s financial system. This is not a passing campaign; it is a core part of the nation’s economic strategy.

The Safe and Wise Path: How to Send Money Legally

Just as the coffee ceremony has its proper, beautiful steps, so does sending money. Following the right path ensures your gift arrives safely and brings only joy, not trouble. The government has made it easier than ever to use formal channels.

Your Secure Options

I have sent money to Ethiopia a couple of times. The fastest and easiest way is to use the recipient’s bank account or international money transfer companies.

Here are some of the most common and trusted options available to the diaspora:

- Major International Money Transfer Operators (MTOs): Companies like Western Union, MoneyGram, and RIA have extensive networks of partner banks and payout locations across Ethiopia.

- Digital and Mobile Remittance Services: A growing number of digital platforms are licensed to operate. Telebirr Remit, the international arm of Ethiopia’s largest mobile money service, is a prominent example. Many other global fintech companies are also on the NBE’s approved list.

- Direct Bank Transfers: You can send money directly from your bank account abroad to a recipient’s account in an Ethiopian bank. While this can sometimes be slower, it is a very secure method.

How to Verify? Before using any service, visit the National Bank of Ethiopia’s official website (nbe.gov.et) and check their published list of licensed money transfer agents. The page is typically found under a URL like nbe.gov.et/mta/.

A Final Word from Your Guide

Ethiopia is a beautiful country to visit and spend time, whether for family reasons or investment purposes. Coming to Ethiopia is a chance to reconnect with the land, with family, and with shared heritage. It is a time for celebration, not for navigating legal complications or worrying about a frozen bank account.

The few extra Birr promised by the black market are not worth the risk to your peace of mind or the security of your loved ones. The government’s resolve is firm, its tools for detection are sophisticated, and the consequences are real. Choose the path of wisdom. Use the licensed, legal channels that protect you, protect your family, and contribute positively to the nation’s growth.

May your visit be blessed, your reunions joyful, and your generosity a source of pure happiness. Welcome home.

Ethiopias Mega Airport to Reshape Africa | BIG Investment Opportunity, HURRY!